Why Is Medicare Advantage So Popular? A Real Life Squid Game

TL;DR: Medicare Advantage (MA) is so popular and growing because of the increase in Medicare enrollees, the intricate business model based on overpayments, risk-score gaming, and relationships with healthcare providers. The Medicare Gold Rush, involving billions of dollars in recent investments, is linked to these dynamics, creating a distorted market that ultimately drains taxpayers and obstructs serious healthcare reform. The Medicare Advantage game is a way some health companies make extra money by taking advantage of the rules in the Medicare system. They do this by finding more health issues to report, getting paid more from the government, and then using those extra payments to offer more attractive insurance plans to seniors. The government pays more than it should for these plans, while the involved companies make a bigger profit. This game includes companies paying doctors to report more health problems, sharing the extra money with doctors, and even owning the doctor's offices. However, it's important to remember that not all Medicare Advantage plans are part of this game.

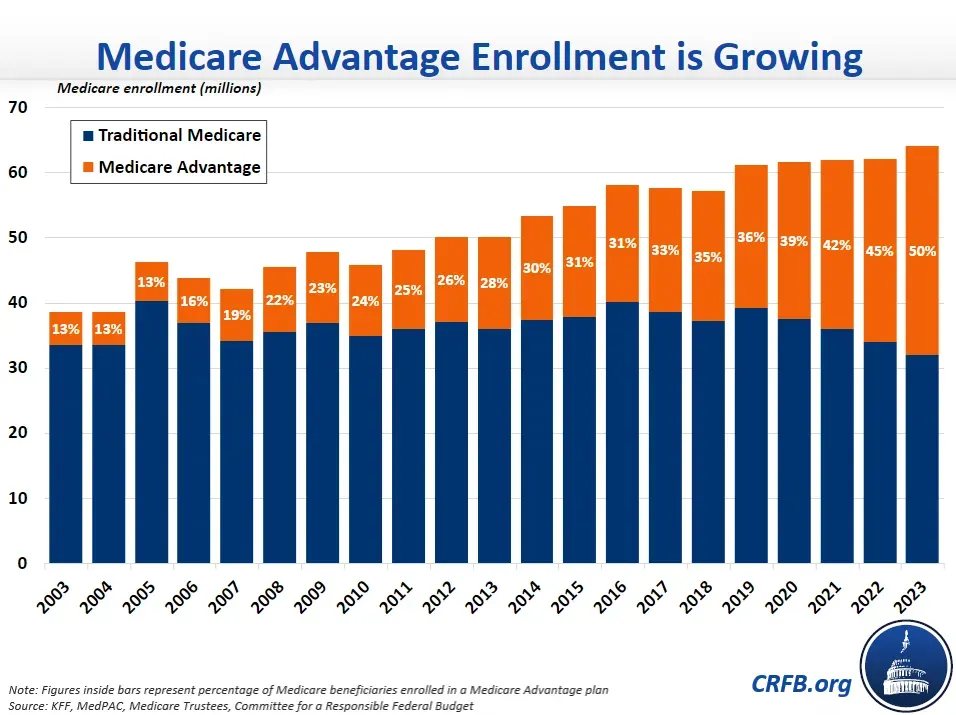

What percentage of Medicare is private today?

Medicare Advantage (MA) plans have gained traction, with enrollment nearly doubling in the past 15 years. As of 2023, 49% of Medicare enrollees are enrolled in privatized Medicare or Medicare Advantage over traditional fee-for-service (FFS) Medicare. Although this growth is often attributed to the private sector's efficiency and cost-saving abilities, closer examination reveals that factors like induced utilization, legislated payments, and risk-score gaming contribute significantly to MA rebates and profitability. As MA plans continue to grow, they represent a shift towards privatizing healthcare in the US.

Data suggests that risk scores in MA plans are approximately 8% higher than in FFS, despite no evidence of worse health conditions. This risk score inflation results in an overpayment of about $10 billion annually, casting a shadow on the apparent savings in MA plans.

Why is Medicare Advantage so popular?

1. Increase in Medicare Spending and Predicted Growth in Baby Boomers

One of the primary drivers behind the boom in Medicare Advantage is the expected rise in Medicare spending. Over the next ten years, spending is anticipated to double from $800 billion in 2019 to $1.6 trillion in 2028 as Baby Boomers age. This demographic shift creates an attractive investment opportunity for healthcare organizations and investors alike.

2. Lots of Money To Be Made Due To Overpayments

Over the past 12 years, the Medicare Payment Advisory Committee (MedPAC) has documented approximately $140 billion in MA overpayments. Risk-score gaming in MA leads to CMS consistently overpaying MA Plans with little-to-no demonstrable clinical benefit to patients. The inflated HCC risk scores allow MA plans to draw enormous overpayments by submitting diagnosis codes, enabling MA Plans to maximize profits without necessarily improving patient care. These overpayments create heavily subsidized and distorted market dynamics that contribute to the rise of MA.

3. Convoluted Dynamics of Costly Plans = Easier to Sell

The market dynamics in MA are perverse due to the overpayments received by MA Plans are being used to bolster the extra benefits to make it more attractive to consumers. Consequently, the more costly a plan is to the payer (CMS), the easier it is to sell to the consumer and the greater the profit. These subsidized dynamics have led to significant start-ups in healthcare, creating a pillaging effect in the industry, with healthcare providers and insurers capitalizing on the financial gains generated from these overpayments.

4. Direct Contracting: The Ultimate Catalyst

The Trump administration introduced Direct Contracting as a new financial intermediary between CMS and non-MA beneficiaries. The aim was to move traditional Medicare beneficiaries into fully capitated, privatized Medicare coverage. This launch has provided an added boost to the MA boom, as organizations are encouraged to tap into the billions of dollars in traditional Medicare spending that would otherwise be directed towards fee-for-service (FFS) beneficiaries.

This new model inadvertently converts traditional Medicare beneficiaries into Medicare Advantage-like arrangements without consent or knowledge.

Get affordable doctor copay without paying insurance premiums

Join 39,000 people and get Mira, the best alternative to traditional insurance. Enroll and use immediately. Plans start at only $45/mo.

Khang T. Vuong received his Master of Healthcare Administration from the Milken Institute School of Public Health at the George Washington University. He was named Forbes Healthcare 2021 30 under 30. Vuong spoke at Stanford Medicine X, HIMSS conference, and served as a Fellow at the Bon Secours Health System.