I woke up the other day to a slew of text messages asking: "Did you see that executive order?" Most days, this might set off some alarms, but I had already seen the news. On June 24th, President Trump signed an executive order mandating hospitals and insurers to "publish prices that reflect what people pay for services." Notably, this latest directive aims to improve pricing transparency in healthcare.

Earlier this year though, the CMS, the largest government-sponsored payor in healthcare, required hospitals to publish charge prices, which meant little to the average consumers, especially considering that insurers rarely pay the full price to begin with.

As the go-to healthcare guy, I get a lot of questions ranging from which hospital to go to, to how to make medical bills go away - which I wish I knew the answer to! In particular, I get asked about pricing almost once a day, so let's dive deeper into that topic now...

For non-healthcare folks, here's how pricing works when you go to the hospital or the ER

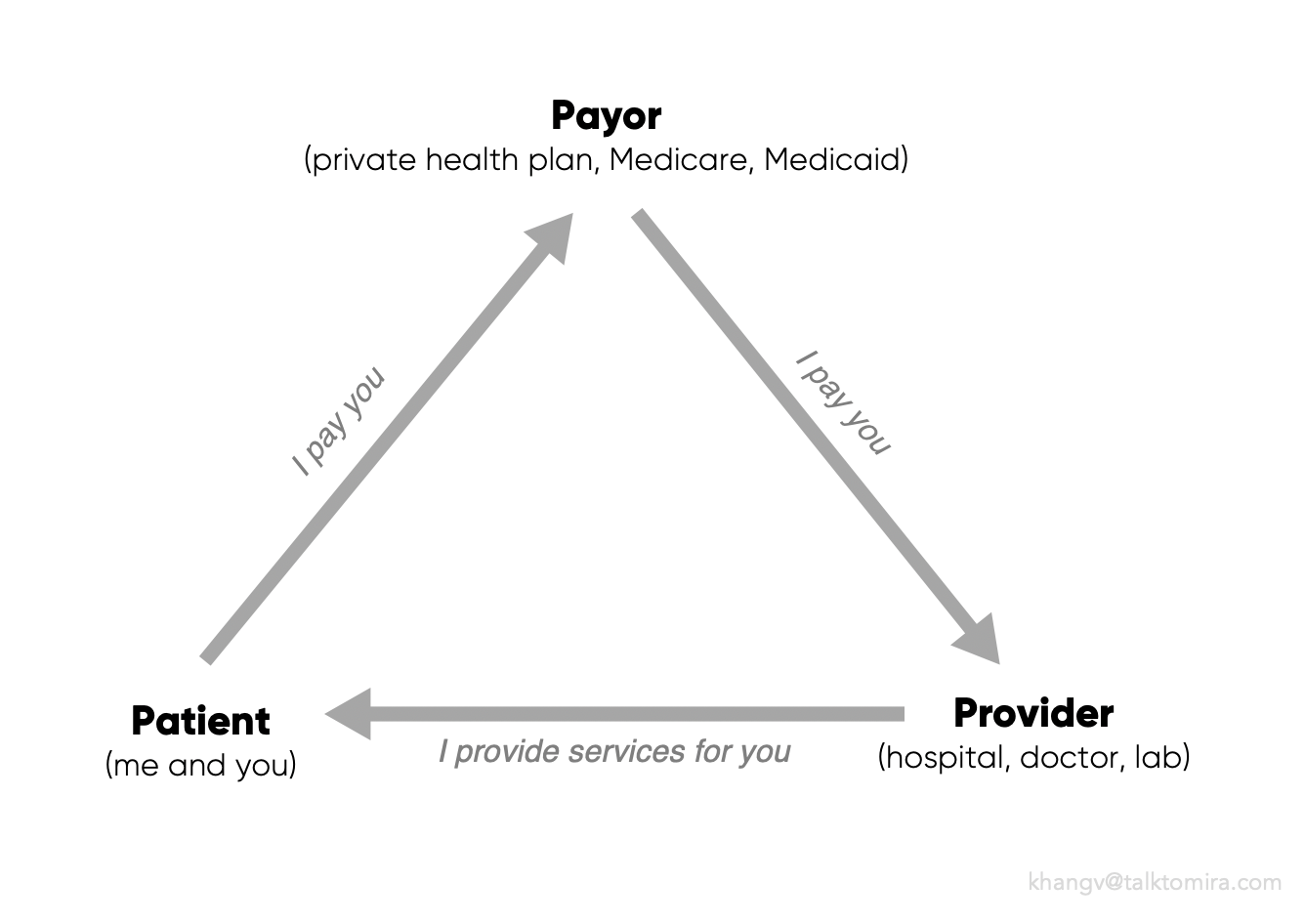

The first step is to understand the healthcare triangle.

Unlike going to the grocery store, in most cases, you're unable to "buy" healthcare yourself. Instead, you pay into a pool of cash, which is your insurance, with the hope that if something catastrophic happens, your insurance will cover it.

Working on your behalf, the insurer negotiates with hospitals to get you the best discounts off of the charge/full prices...supposedly.

While overly simplified, the triangle below depicts the three main stakeholders in a healthcare ecosystem (with suppliers and pharmaceutical companies excluded from the picture):

The second step is to understand why what you see is not what you pay.

Charge price, reimbursement, Medicare price. What the heck are those?

The best way to think about hospital pricing is through an analogy using Starbucks' menu. I know, it sounds weird, but bear with me. (No endorsement here :P)

Let's consider the Frappuccino, there are three tiers of “product” you can get:

- Venti (large)

- Grande (medium)

- Tall (small)

Venti: this is the "charge price," the highest price that the hospital uses as its starting point for negotiation - kept secret in a menu called the "charge master"

Grande: insurers negotiate with hospitals to pay a portion of the full price, often 30-40%

Tall: Medicare and Medicaid, as the largest government-sponsored payor, dictate how much they want to pay - often 10–20% for Medicare and less for Medicaid.

The difference here though: when you go to Starbucks, the more you pay, the more Frappuccino you get. In healthcare, a knee replacement might cost your grandma's Medicare ~$15K, but could cost your private insurance over $25K.

So, if you don't have insurance, what do you pay?

Unfortunately, without someone to negotiate on your behalf, uninsured patients often get billed the full charge price, which can be three times more expensive. In the case of the knee replacement, full charge can be about $80‚Äì150K. Discounts are sometimes available, but can‚t be negotiated ahead of time.

If I have insurance, why do I still have to pay so much out of pocket then?

This is a complicated question depending on who you ask, but it basically comes down to two things:

- Price inflation: As hospital and drug prices go up, insurers have to pay more for the same care you receive, which makes them less profitable or even incur a loss. To counter this force, many insurers want the customers to have more skin in the game.

- Cost sharing: To do this, insurers increase deductibles (the amount you have to pay before the insurance starts paying) or implement a co-pay (you share the cost with them for each visit), in the hope that people will shop around for the best deal and wisely choose which hospital to visit.

The problem with this is that you can‚t shop without knowing prices.

Real prices are kept secret by hospitals and insurers, which they don't want to share, even with internal staff. Consequently, healthcare consumers continue to do what they do best: go wherever is most convenient at the time.

In 2019, the annual cost for an individual health plan is upwards of $4000 with a ~$7000 deductible (what you pay before insurance pays for healthcare services). In other words, for a bad year, you're looking at an $11000 out of pocket expense if something catastrophic happens. And even if nothing happens, that $4000 is still gone from your paychecks.

Are there any solutions?

According to the latest data, 30 million Americans are without insurance, while another 56 million have insurance but are underinsured. This is a widespread issue that affects many peoples' lives and has the power to swing political elections. Solutions are being proposed by candidates and lawmakers everyday, but here are my thoughts:

- High deductible health plan: we tried this, pretty much a problem on its own. If you have it, you know it.

- Medicare For All: the current federal budget for healthcare stands at $1 trillion dollar. There are approximately 2.6 million people employed by the insurance industry. A single payor system would drive down prices, but physicians are likely to oppose the idea since a centralized negotiation power would significantly reduce reimbursement.

- 100% Privatization of Healthcare: most people are unaware, but 29% of the Medicare budget ( $700B) is already being administered by private carriers, known as Medicare Advantage - this is one of the hottest segments in healthcare. Privatizing healthcare does increase competition, which improves patient experience. However, privatizing healthcare also prioritizes profits over social programs, which will likely play out unfavorably for those who live in the bottom 20% of the income scale. Prices, on the other hand, will probably stay the same.

Lastly, for the consumers, what do you do? The most innovative approach I have seen so far occurs in Kansas City. A group of doctors converted to 100% cash, cutting out the middlemen, and passing the savings to the patients. Many are following suit across the country in a movement called Direct Primary Care. Direct payment is not new, however, it is only known to those who are in the “inner circle.”

Next time you're at the pharmacy, it's worth asking for cash prices with coupons. Your Z-pack that costs $50 with insurance might magically become $5, but only if you ask....