The average individual premiums in 2024 for the U.S. is $456. depending on multiple factors. Your insurance plan varies by metal tier and plan type. Millions of people are without insurance or pay out of pocket for healthcare services, so obtaining a plan from the Marketplace can be an excellent option for many. There is a federal Marketplace, but many states also offer their individual health insurance.

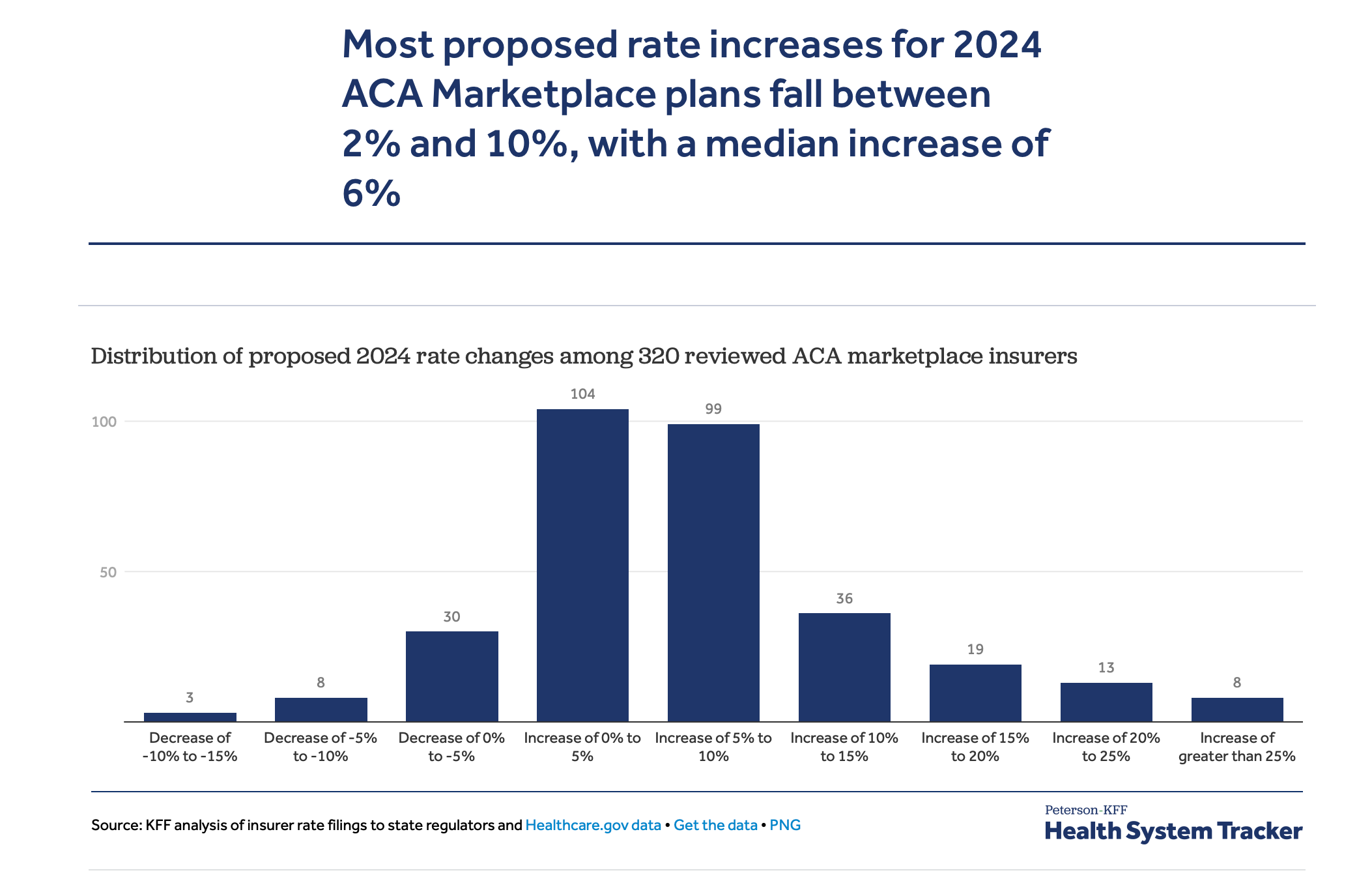

Recent analysis found that insurance premiums are expected to increase an average of 6% (again) for 2024. Researchers cited three main factors that drive premium increase: inflaiton, end of COVID-19 related Public Health Emergency, and unwindling Medicaid enrollment.

An alternative to individual health insurance plans is health memberships such as Mira. If you are struggling to find affordable yet high-quality health coverage, you may want to consider Mira. For as little as $45 a month, Mira members get access to low-cost virtual and urgent care, up to 80 percent off select medications, and same-day lab testing. Sign up for Mira today and get covered today!

Metal Tiers & Cost of Individual Health Insurance Plans Across the U.S.

There are four types of individual health insurance plans: bronze, silver, gold, and platinum. However, platinum plans are pretty rare in the health insurance Marketplace. The tier you choose will affect the total cost of your premium - the amount you pay for your health insurance each month. Silver and Gold insurance plans will cost more monthly. Still, your insurance company will pay a more significant percentage of the cost of medical bills, 70% and 80%, respectively. Healthcare.gov outlines the similarities and differences and which plan might be more applicable to you here.

The following table has been adapted from the Kaiser Family Foundation depicting the average lowest-premium cost for a 40-yr old per state by metal tier for the year 2023.

| Location | Average Premium 2023 |

|---|---|

| United States | $456 |

| Alabama | $567 |

| Alaska | $762 |

| Arizona | $410 |

| Arkansas | $416 |

| California | $432 |

| Colorado | $380 |

| Connecticut | $627 |

| Delaware | $549 |

| District of Columbia | $428 |

| Florida | $471 |

| Georgia | $413 |

| Hawaii | $469 |

| Idaho | $420 |

| Illinois | $453 |

| Indiana | $397 |

| Iowa | $484 |

| Kansas | $471 |

| Kentucky | $422 |

| Louisiana | $565 |

| Maine | $457 |

| Maryland | $336 |

| Massachusetts | $417 |

| Michigan | $362 |

| Minnesota | $335 |

| Mississippi | $461 |

| Missouri | $473 |

| Montana | $477 |

| Nebraska | $550 |

| Nevada | $386 |

| New Hampshire | $323 |

| New Jersey | $441 |

| New Mexico | $445 |

| New York | $627 |

| North Carolina | $512 |

| North Dakota | $475 |

| Ohio | $413 |

| Oklahoma | $510 |

| Oregon | $462 |

| Pennsylvania | $433 |

| Rhode Island | $379 |

| South Carolina | $496 |

| South Dakota | $626 |

| Tennessee | $473 |

| Texas | $461 |

| Utah | $471 |

| Vermont | $841 |

| Virginia | $371 |

| Washington | $395 |

| West Virginia | $824 |

| Wisconsin | $456 |

| Wyoming | $802 |

Source: Kaiser Family Foundation

Metal tiers have nothing to do with the quality of care you will receive. They determine how you and your plan split your health care costs. The table below, adapted from the Healthcare.gov website, lists the responsible percentage of medical costs that both your insurance company and you will be responsible for based on the metal tier.

Cost Splitting Between Insurance Company and You Based on Plan Type

Plan | Best Suited For | Insurance Company Covers: | You Cover: |

|---|---|---|---|

Bronze | those who are fit and healthy and want to protect themselves from worst-case medical scenarios | 60% | 40% |

Silver | those who might need a little more medical attention than the average person | 70% | 30% |

Gold | those who will need frequent access to care (e.g., chronic conditions)

| 80% | 20% |

Platinum | those who will need frequent access to care and are willing to pay higher premiums in exchange for the majority of medical expenses covered | 90% | 10% |

Source: Healthcare.gov

Factors that Influence the Cost of Individual Health Insurance

Several factors contribute to the total cost of individual health insurance. These include your location, age, tobacco consumption, family size, metal tier, network type, and the savings and credits you are eligible to receive.

Location, Age, Tobacco Use, & Family Size

Health insurance rates vary based on geographical location and providers available in the respective regions. Higher insurance rates are associated with older age and the number of people covered under it. Some states factor tobacco use into the price of insurance, where you could pay up to 50% higher rates if you smoke.

Metal Tier & Network Type

The type of health plan you have will affect your deductible and copay, as will the tier type. The three major plan options are Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), and Point of Service Plans (POS). These plans use a network of doctors and hospitals; the chosen plan will determine how broad or narrow your network is. This usually correlates with how high the monthly premium is. Suppose you want more available health care professionals covered under your insurance. In that case, you will likely be paying more every month.

As mentioned earlier, there are four different metal tiers when it comes to individual health insurance. Each provides different levels of coverage and, therefore, comes with other monthly premium totals. Suppose you plan on utilizing lots of medical services. In that case, you may choose a plan that costs more but covers a more significant percentage of your medical costs. Inversely, if you do not intend on using medical services often, you may opt for a cheaper plan. However, you will find yourself paying a more significant percentage of your medical costs.

Tax Credit & Cost Saving Reduction Eligibility

Another major factor in the cost of your Marketplace plan are the tax credits and cost-saving reductions (CSRs) you may be eligible for. When you complete an application and enroll in a health insurance plan through the Marketplace, you will find out whether you qualify for this credit. The table below defines the two terms based on the Healthcare.gov glossary.

| Premium Tax Credit | “A tax credit you can use to lower your premium when you enroll in a plan through the Health Insurance Marketplace.” |

|---|---|

| Cost Saving Reduction | “A discount that lowers the amount you have to pay for deductibles, copayments, and coinsurance. In the Health Insurance Marketplace, cost-sharing reductions are often called ‘extra savings.’” |

Your tax credit is based on the Marketplace application you submit. You qualify for tax credits if your income is between 100 to 400 percent of the federal poverty level (FPL) in all states. You must enroll in a plan in the Silver category to use any CSR you may be eligible for. The promising news is that most who apply for a Marketplace plan will qualify for some amount of savings.

The Marketplace

You can purchase individual health insurance on-exchange or off-exchange. However, most purchase their health insurance on-exchange, meaning through the federal health insurance Marketplace. The federal health insurance Marketplace is the government website where you can browse various health care plans available under the Affordable Care Act (ACA).

There is health insurance available for every state. Still, some states vary regarding how they manage their health insurance exchanges. For example, DC and 17 other states exclusively use state-run marketplaces. If you lived in one of these states, you would purchase a health insurance plan through the state's specific enrollment website. The territories and states that utilize state-run Marketplaces include:

- California

- Colorado

- Connecticut

- District of Columbia

- Idaho

- Kentucky

- Maine

- Maryland

- Massachusetts

- Minnesota

- Nevada

- New Jersey

- New Mexico

- New York

- Pennsylvania

- Rhode Island

- Vermont

- Washington

Buying an individual health insurance plan off-exchange is also an option. This is where you would buy a health insurance plan directly from an insurance company or broker. These plans will still be ACA-compliant but will not be purchased using the federal or your state’s Marketplace. Finding a plan off-exchange is usually a more direct way to obtain a health insurance plan as you speak directly to insurance representatives. However, one benefit of purchasing your plan on-exchange is that you may be able to qualify for financial help and receive tax discounts to save on total costs. Some on-exchange plans offer premium subsidies (premium tax credits) and cost-sharing reductions (cost-sharing subsidies).

Affordable Care Act

The ACA, also called Obamacare, made it mandatory for each insurance plan offered on the Marketplace to cover 10 essential health benefits, such as preventative, maternity, and rehabilitative care. The ACA extended health insurance coverage to millions of Americans previously uninsured when President Obama passed it into law in 2010. This made it so that health insurance companies could not refuse to cover you or charge you a higher premium because you have a “pre-existing condition” such as cancer, diabetes, or another chronic health condition. The 10 essential health benefits covered include:

- Prescription drugs

- Outpatient services

- Emergency services

- Hospitalization

- Maternity and newborn care

- Mental health and substance use disorder treatment

- Rehabilitation services

- Laboratory tests

- Preventive care

- Pediatric services

Eligibility

Anyone who does not have access to employer-sponsored or government-run (e.g., Medicare) health coverage can potentially be eligible for individual health insurance. Other eligibility requirements include:

- Living in the United States

- Being a U.S. citizen or national (or being lawfully present)

- Not being in prison

The Marketplace was designed to lessen the amount of uninsured Americans. Therefore, just about any American citizen is eligible. On the Marketplace, you can compare plans based on price, benefits, quality, and other important features before purchasing a plan. When you submit your application, you will also find out if you are eligible for Medicaid or Children's Health Insurance Program (CHIP).

If you are not eligible for individual health insurance, Mira may also be a great option. With Mira, you can access urgent care visits, lab testings, and up to 80% off on over 1000 prescriptions for a low cost of just $45 per month.

Open Enrollment Periods & Qualifying Events

When choosing a Marketplace plan, you must do this specific period, called the open enrollment period. Open enrollment usually occurs in the fall, when you purchase and enroll in a health insurance plan for the following calendar year. Suppose you need health insurance but find that the open enrollment period has already passed. In that case, you may still be eligible to sign up if you have experienced a qualifying life event. There is a special enrollment period if you experience a qualifying life event (QLE). Healthcare.gov defines a QLE as “a change in your situation that can make you eligible for a Special Enrollment Period, allowing you to enroll in health insurance outside the yearly Open Enrollment Period.” Examples of qualifying life events can include:

- A change in residence

- Becoming a U.S. citizen

- Leaving jail or prison

- Changes in household structure

- Job Loss

- Loss of eligibility for Medicare or Medicaid

- Aging out of parent’s health insurance plan

- Getting married

- AmeriCorps members starting or ending their service

- More

Cost of Individual Health Insurance Frequently Asked Questions (FAQs)

Consider this additional information when it comes to the cost of individual health insurance.

How Do I Choose The Right Marketplace Insurance Plan for Me?

You can start by determining your health needs. You can use the Marketplace to “shop around” and compare different plans. This comprehensive article provides information to keep when determining if a Marketplace plan is right for you. It is vital to keep your budget in mind and look not just at the monthly premium prices but also consider co-pays, coinsurance, and out-of-pocket maximums. This Marketplace tool allows you to browse plans specific to your and your family’s medical needs.

Can I Enroll in an Individual Health Insurance Plan Even If My Employer Offers Insurance?

Yes, you can; however, employer-sponsored health insurance is usually the cheapest option. Employers will typically cover part of the insurance premiums from your employer-sponsored coverage. If you choose a Marketplace plan, you will be responsible for paying the total cost of the premiums. Additionally, choosing a Marketplace plan over an employer-sponsored plan could mean you lose out on the subsidies most are eligible for on the Marketplace. Unless your employer-sponsored insurance does not meet the ACA’s minimum standards.

Do I Need To Re-Enroll the Following Year If I Want the Same Plan?

If you do not do anything, you will automatically be auto-enrolled in the same plan the following open enrollment period.Suppose your current health plan will not be offered the next year and you do not do anything. In that case, your insurance company will automatically enroll you in another policy that is similar to the one you currently have. Even if you plan on enrolling in the same plan, it is a good idea to log onto your Marketplace and update any financial or medical information, as this could adjust the price of your plan.

Bottom Line

Many have enrolled in an individual health insurance plan through the federal or their state’s Marketplace. There is great variation in your monthly costs and premiums based on your plan type. Paying more monthly correlates with greater insurance coverage for medical costs. Multiple factors contribute to the total price of an individual health insurance plan. You can only enroll in a plan during the annual open enrollment period unless you qualify for an exception with a qualifying life event.