According to the World Bank, healthcare spending in the U.S. was $10,586 per person in 2018. In the same year, the median household income was $63,179. This means one out of six dollars spent was in healthcare, whether it was through health insurance premiums, copays, or tax payments.

Another study from the Massachusetts Health Policy Commission found 40 cents of every additional dollar earned in the past ten years was canceled out by rising healthcare costs.

One solution to address this unsustainable rise in healthcare expenditures relative to income has captured the zeitgeist recently, known simply as “Medicare for All”. What is less clear is how such a program would operate, what it would mean to you in terms of out-of-pocket costs and possible monthly premiums.

A Recap of The U.S. Healthcare Industry In 2020

- The national U.S. healthcare expenditure is $3.6 trillion in 2019 and is projected to reach $6.0 trillion in 2027 - nearly double

- The federal government spent $750B on the current Medicare program - 15% of the government budget

- The national deficit (debt) is standing at $17.2 trillion as of January 2020, larger than the economy as a whole

- Healthcare as a sector employs over 16 million people - one out of ten jobs in the U.S>

- Health delivery (hospitals and doctors) alone contributed to 29% of job gains from 2001 to 2016

- In 2020, employers estimate the cost of healthcare coverage to reach $15,375 for every worker and their families

- There are 30 million people without insurance and 56 million people who have insurance but can't afford to use it

The big picture: it is undeniable that U.S. healthcare is expensive. But it is also one of the main driving forces behind American economic prosperity. In a sense, we all are paying for prolonged economic growth with rising healthcare costs.

Is Medicare Free?

Medicare, unlike most people think, isn't entirely free.

There are three types of Medicare:

- Part A (for hospital) is free if you paid more than 7.5 years of taxes

- Part B (for doctor visits) costs $144 a month

- Part D (drugs) costs $34 a month.

On average, you can expect to pay $178 a month if you're qualified for Medicare. Let say you just came to the U.S. at 65 and have not paid taxes for more than 7.5 years, your monthly premium would be $178 + $458.

2020 monthly premium for Medicare

The Idealistic Vision: Free-For-All

A single-payer, government-run healthcare program that covers all Americans. This program will replace all private and public health insurance and will be financed with a mandated tax premium paid by employers and individuals.

Medicare For All will lower administrative costs significantly by consolidating all insurance activities under one roof. This program will also be free to all citizens at no monthly cost. All services are covered, from primary care to hospital stays, and even minor cosmetic surgeries.

Drug prices will be reduced by half because the U.S. Department of Health will become the largest purchaser on earth with the greatest power to negotiate.

An idealistic vision for Medicare for All

But, How Will We Pay For It?

Increase individual and payroll taxes - most likely. Currently, 2.9% of your federal taxes is for Medicare. To expand this program three to four times and cover everybody, the current tax rate for Medicare will also likely triple or quadruple. This means one could see his or her tax go up to 7% to 10% regardless of the income bracket.

Tax the top 10% more - tricky. Instead of increasing tax for everybody, one other solution would be to increase income taxes for the 10%. What we found, however, is that the majority of high net worth individuals in the U.S. generate their wealth by long-term capital gains (investment) instead of pure salary.

The government could increase the capital gain tax above 20%, but that would have an even bigger implication for the U.S. economy at large. Considering the stock market survival relies solely on capital gains, this would put the entire economy back in recession.

Increase corporate tax - not viable. U.S. corporate tax rate was reduced from 35% to 21%. Even at the previous level, financing Medicare for All would not be possible since corporate income taxes only make up a small proportion of the total federal government revenues as a whole.

Increase corporate taxes seem like a good option but is not a viable one considering it is a smaller proportion of U.S. government revenues

The More Probable Vision: Expanded ObamaCare + Medicare Advantage

Over 35% of Medicare is administered by private carriers via a product called "Medicare Advantage" - the fastest-growing segment of Medicare. Under Medicare Advantage, enrollees may get more perks like a gym membership, virtual care, and so on.

But while Medicare Advantage is still technically Medicare, it is not entirely free either. The US Department of Health pays private insurers $800-$1200 a month to manage each Medicare member on their behalf.

There is also one other public option - individual exchange aka Obamacare.

The more probable scenario for Medicare for All to happen is a blend of Medicare Advantage and ObamaCare - where the federal government will give money to private insurers to make ObamaCare more available to the public and increase the income limit for the subsidy.

A less extreme version of Medicare for All: an expanded public option

How Much Will Expanded Medicare Cost?

A public experiment at this scale has never been done since President Franklin D. Roosevelt signed into law the Social Security Act in 1935, but one good benchmark would be the average cost of products on the individual exchange.

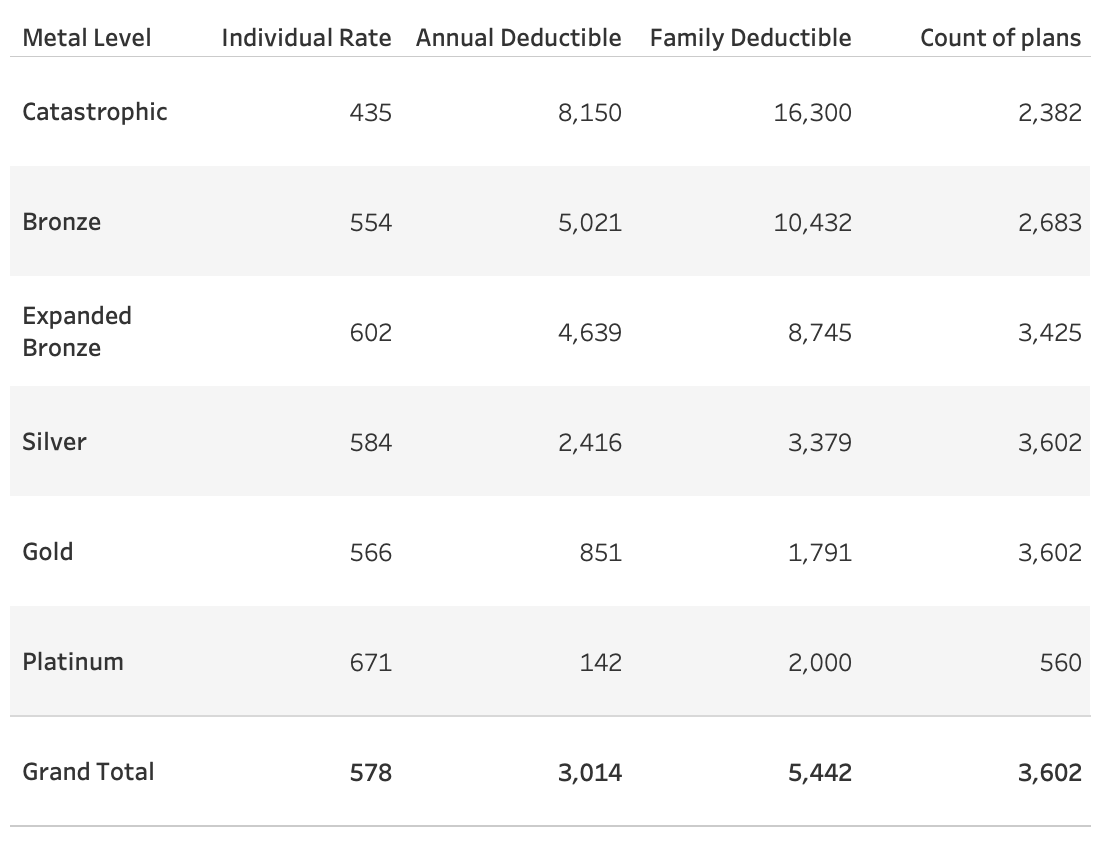

For 2020, the average cost for health insurance on the individual exchange is $435-$671 with a $3000+ deductible. Using this as a proxy, we can safely say that an Expanded Medicare will likely cost the same or less with subsidies.

In the Medicare for America Act from Reps. Rosa DeLauro (D-Conn.) and Jan Schakowsky (D-Ill.), out-of-pocket costs for lower-income individuals would be zero, but people in higher income brackets would pay more: up to $3,500 in annual out-of-pocket costs for individuals or $5,000 for a family - this aligns with the current cost level for exchange products.

Given the individual mandate (tax penalty) was effectively repealed by Congress and the stark resisting attitude toward ObamaCare, an expanded public option would have a very slim chance of passing both houses.

2020 Individual Exchange rates

A Compromise: A Universal Catastrophic Option

Some states already have a public catastrophic plan called reinsurance. These are "insurance" for insurers, effectively cap the claim payment amount when it reaches a certain level.

Alaska began operating a reinsurance program in 2017. Oregon and Minnesota joined them in 2018. Wisconsin, Maine, Maryland, and New Jersey have reinsurance programs as of 2019. Several other states, including Colorado, Delaware, Montana, North Dakota, Pennsylvania, and Rhode Island are working to implement reinsurance programs that will take effect in 2020 or 2021.

For example, in Maine, the MGARA reinsurance program will pay 90% of claims that are between $47,000 and $77,000, and 100% of claims that range from $77,000 up to $1 million.

While this is not a consumer-facing program, the same mechanism could be used to build a national catastrophic plan supported by both houses.

States with reinsurance programs

What Will A Universal Catastrophic Option look Like?

In a compromise, Congress will expand the current pool of reinsurance cash to cover all 50 states.

There will be an ultra-low or zero premium catastrophic plan that covers everybody for medical procedures over $20K like baby delivery, surgeries, and episodic care for chronic illnesses. This number is arbitrary but a more robust actuary model can help figure out what's the right threshold.

Another source of cost-sharing could come from the consumers. Let say 250 million adults (and their employers) pay an average $100 monthly premium, that's a $300B annual pool of cash that could be used toward establishing a bigger national reinsurance program in the near term.

By aggregating demand of highly expensive procedures under one roof, the federal government could negotiate better rates with mega health systems and lower reimbursements as well as reduce the administrative burden associated with billing multiple health plans.

This option would not do away with private insurance. By having a two-tier system, those with both private insurance and catastrophic plan will pay near-zero copay. Those without insurance will have to pay out-of-pocket, but won't be stuck with hundreds of thousand of dollars for emergency care or hospitalization.

A universal catastrophic option could pass both the financial and political tests

The Bottom Line

Healthcare is complex and the business of healthcare is even more so. Universal healthcare programs like that of the U.K. and Canada are less likely to work given the existing industry structure and the scale of U.S. healthcare.

We looked at both extreme and least extreme scenarios for Medicare for All and found a compromise that works - a universal catastrophic plan. One could expect to pay $100 a month for catastrophic coverage to cap your medical expenses at a certain threshold. This program could also be free for low-income people with subsidies.

By expanding a relatively bipartisan program (reinsurance) to cover expensive medical procedures that exceed a certain threshold, we could extend protection to all Americans at a reasonable cost without doing away with private health insurance.

People who love their insurance can keep them and pay near-zero out-of-pocket. Those without insurance will have to pay more but won't be bankrupted by the enormous cost of hospitalization or emergency care.

As compromise being the American constitutional tradition, we think it may also apply in healthcare.

I realize this is a very complex topic with many nuances. This article is by no means a perfect prescription to fix U.S. healthcare. I welcome comments and opinions should you want to chat khangv@talktomira.com.